EUDR Supply-Chain Intelligence

Six months before the new EUDR deadline

What has really changed since December 2025, and what has not

Between 18 December 2025 and March 2026, three law-firm briefings were written on the same matter, the second EUDR postponement, and arrived at three very different tones. Covington & Burling read the revision technically: “published in Official Journal”, deadline tables, new thresholds. Norton Rose Fulbright read it structurally: what the simplifications actually shift in terms of obligations. KPMG Law read it operationally: “What does your sustainability team concretely have to do?” All three readings are right. None suffices on its own.

At myBytes, over these six months, we kept our satellite monitoring of the West African cocoa-belt regions running on the basis of the two-mask operation, and archived the evaluation snapshots reproducibly in the companion repository on GitHub. The monitoring observes nothing so far that the postponement changed on the ground. The postponement was an act in the Brussels procedure, and it was precisely not an event on a Soubré polygon. From this asymmetry between regulatory choreography and actual growing reality arise three questions that need an answer over the coming six months, up to the new large-operator deadline on 30 December 2026.

This article answers them in turn.

1 · What was actually decided in December 2025

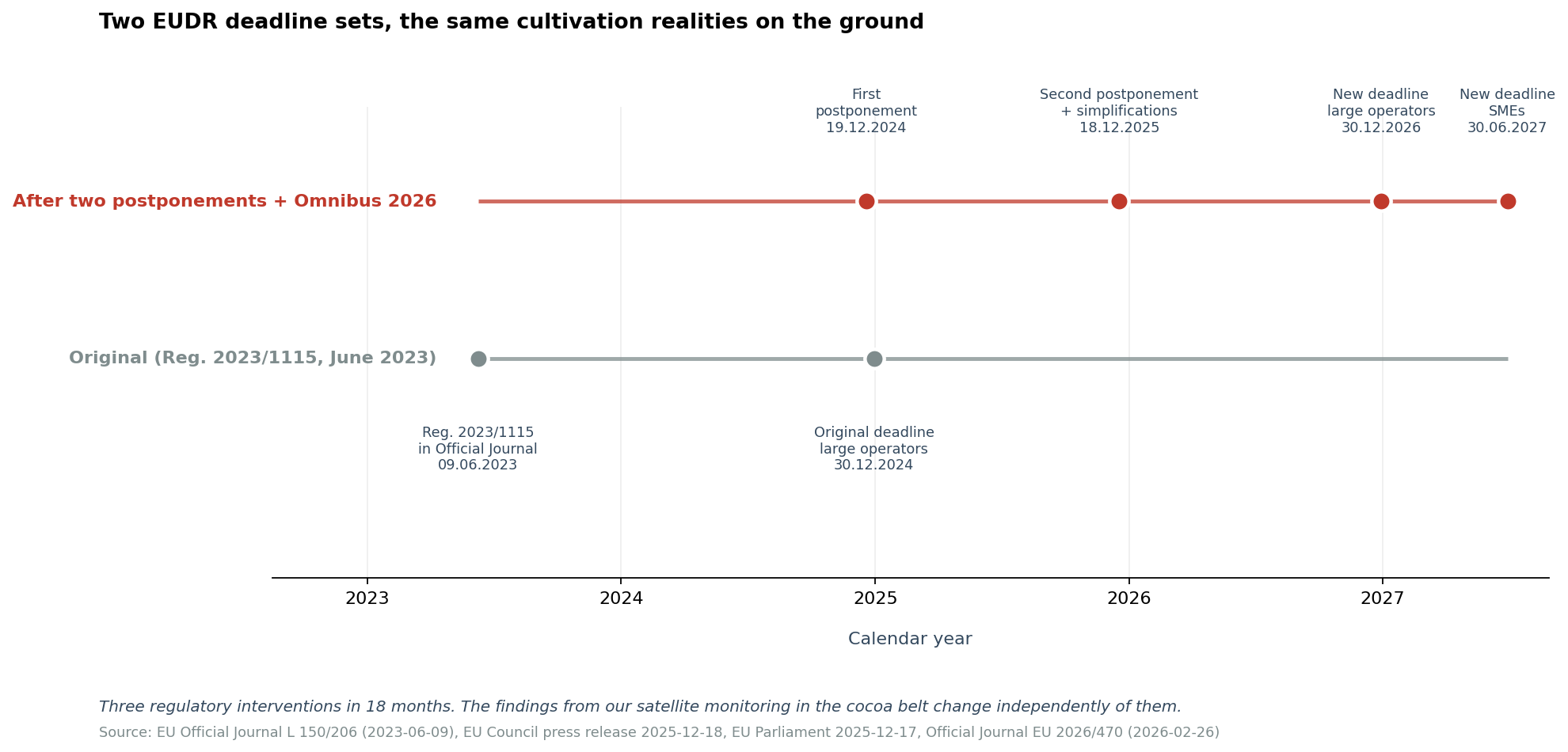

Four concrete changes, all documented in the Omnibus Directive (EU) 2026/470 as well as the preceding Council press release of 18 December 2025 and the European Parliament decision of 17 December 2025 by 405 votes to 242:

First, the postponement. Large operators and traders are subject to application from 30 December 2026, SMEs from 30 June 2027. Both dates are twelve months later than before.

Second, the first-placer simplification. Only the first operator placing the product on the EU market submits the due-diligence statement. Downstream operators and traders are administratively relieved. Anyone who reads this as an “all clear” misses the actual point; we return to it in the section on the first-placer simplification.

Third, printed products out of scope. Publishers and printing houses no longer have to fulfil the regulation separately for their end products.

Fourth, a simplified statement for micro and small operators. A reduced version of the due-diligence statement, technically documented in the Omnibus Directive.

What was not adjusted in December 2025 matters more for the three readings below than what was adjusted:

- The cut-off date of 31 December 2020 under Article 2 remains unchanged.

- The penalty framework of up to 4 % of EU annual turnover under Article 25 remains unchanged.

- The seven commodities in scope (cocoa, coffee, palm oil, soy, rubber, cattle, timber) remain unchanged.

- The burden of proof also remains unchanged: geolocation of each plot plus a documented risk assessment.

So the postponement grants eighteen additional months without the requirement itself becoming a different one.

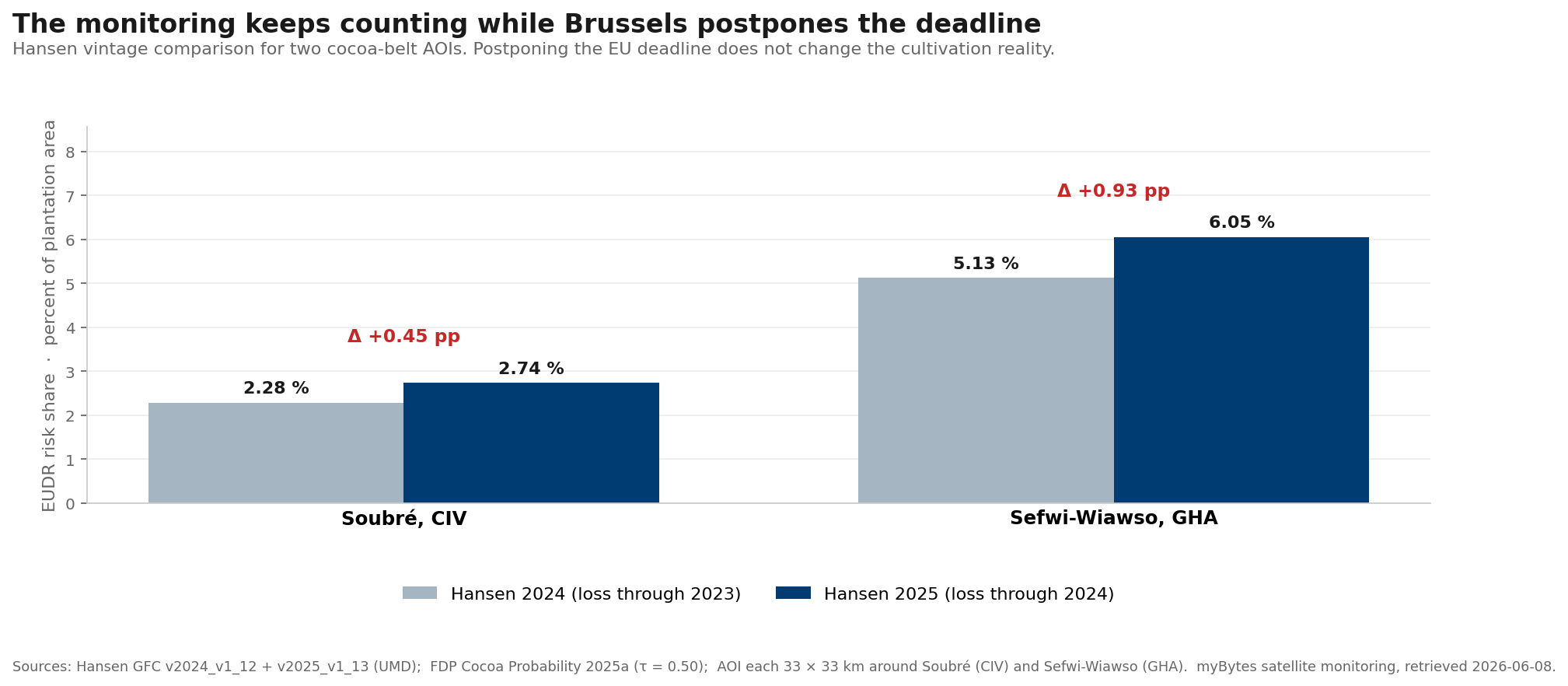

2 · What our satellite monitoring actually shows in the six months since

The numbers above come from two consecutive evaluations of our EUDR satellite monitoring on 8 June 2026, once

against Hansen vintage v2024_v1_12 (forest-loss data through 2023) and once against v2025_v1_13 (forest-loss

data through 2024). Both runs work on the same 33 × 33 km AOI geometry around Soubré and Sefwi-Wiawso

respectively and the same FDP cocoa probability layer (2025a, τ = 0.50). The Hansen layers come from the

public

Global Forest Change dataset (UMD),

the plantation probability layer from the Forest Data Partnership cocoa model 2025a, which builds on the

methodology of

Kalischek et al. 2023 Nature Food.

The methodological operation is described in

our previous article

and implemented in the associated methodology repository

eudr-risk-pipeline.

The concrete drift snapshot of this article is available reproducibly in its own companion repository

eudr-vintage-drift-2026.

Two observations that do not appear when reading the law-firm briefings:

First, the regional topology differs structurally, not just quantitatively. Soubré in Côte d'Ivoire is a smallholder mosaic: many small, scattered forest-loss patches that correlate with low RADD alert activity. Sefwi-Wiawso in Ghana shows geometric large-estate blocks with markedly higher RADD activity over the last 24 months. The eighteen-month postponement does not affect this structural difference. It affects when an importer must fulfil the obligation, not when a farmer plants a pod.

Second, the monitoring values drift measurably upward between the two Hansen vintages. Soubré moves, in the 33 × 33 km AOI, from a 2.28 % risk share (vintage 2024) to 2.74 % (vintage 2025), Sefwi-Wiawso from 5.13 % to 6.05 % (see Figure 2). Both Δ values are small in absolute points, but they show exactly what an operational sensor does: keep counting. The law-firm briefings of February and March 2026 count nothing. They interpret.

3 · Three readings of the postponement, three consequences

The three briefings this article opened with can be tied to three readings. Each is internally consistent. Each leads to a different Q3 2026 decision.

Reading A, the all-clear. Held mainly by providers who sell compliance-monitoring licences and want to keep clients in conversation. Argument: twelve more months, simplified obligations, less pressure on sustainability teams. Weakness: the simplification shifts the burden, it does not eliminate it. Anyone who infers from reading A that the compliance investment can be deferred to Q3 2026 risks no breach of duty in Q4 2026, but certainly a negotiating weakness toward the first placer, who is now at the centre.

Reading B, the new pressure. Held mainly by commercial law firms that lead clients toward compliance programmes. Argument: the postponement buys time, but the detailed obligations (geo-polygons, sensitivity analyses, audit trails) have become more demanding over the eighteen months. Strength: methodologically correct. The burden of proof under Article 10 is unchanged. Weakness: reading B typically ends as a recommendation for a particular provider, not as a methodology for provider selection. It says that methodological depth becomes important, without saying how a buyer distinguishes methodological depth from methodological marketing.

Reading C, the structural problem. Our position. The second postponement is not a symptom of a pragmatic readjustment but a symptom that the compliance world is searching for a methodologically defensible answer, and feels uncertain toward the first wave of providers. A direct piece of evidence is the parallel story of the CSDDD: the original directive (EU) 2024/1760 was substantially postponed and simplified on 26 February 2026 by the Omnibus Directive 2026/470. Transposition by 26 July 2028, application from 26 July 2029, thresholds raised to over 5,000 employees and over EUR 1.5 billion turnover. Two parallel simplification waves in two parallel sustainability directives are no coincidence. They are the consequence of the same market observation: the first wave of compliance providers overwhelmed buyers, and the legislator acknowledged this through simplifications.

From reading C follows a concrete consequence for Q3 2026. Anyone investing in compliance monitoring now buys methodological depth, not a particular deadline date. The deadline shifts; the Article 10 requirement remains.

4 · The first-placer simplification as a hidden risk

We treated the topic at greater length in our methodological EUDR article on the two-mask operation, there in the section “When the first placer falls, the buyers fall with it”. Six months later, what was previously a thesis can be made more precise.

The first-placer simplification shifts the formal due-diligence obligation onto the first operator placing the product on the market. Downstream operators in all seven EUDR commodity chains, that is, consumer-goods manufacturers, food retail and industrial processors, are administratively relieved. Commercially relieved they are not.

Six channels transfer the EUDR risk from the first placer to the buyer:

- Supply discontinuity: a placing ban under Article 24 hits the goods, not the violator.

- Reputational risk: consumer headlines carry brand names, not importer names.

- Force-majeure dispute: supply and purchase contracts must clarify who legally bears the sanction risk.

- Scarcity premium on compliant goods: after the first sanction cases, compliant cocoa becomes a scarcer good.

- Parallel obligation from the CSDDD remainder: for the large enterprises that remain under the CSDDD after the 2026 Omnibus reform, the value-chain due-diligence obligation is still sharp.

- Bank and insurance covenants: first trade-credit insurers such as Atradius and Allianz Trade have included EUDR references in 2026 policy renewals. The exact market diffusion is not publicly and systematically documented; we mark this as known and increasing market practice.

From these six channels follows the actual operational finding: the simplification concentrates the EUDR risk on a single node, the first placer. It makes the buyer paradoxically more dependent on that one node working in a methodologically clean way. Anyone who cannot verify that verifies their own stockout shock after the fact.

That is the core: the simplification shifts the risk from the compliance department into procurement, without procurement having received a new tool for it.

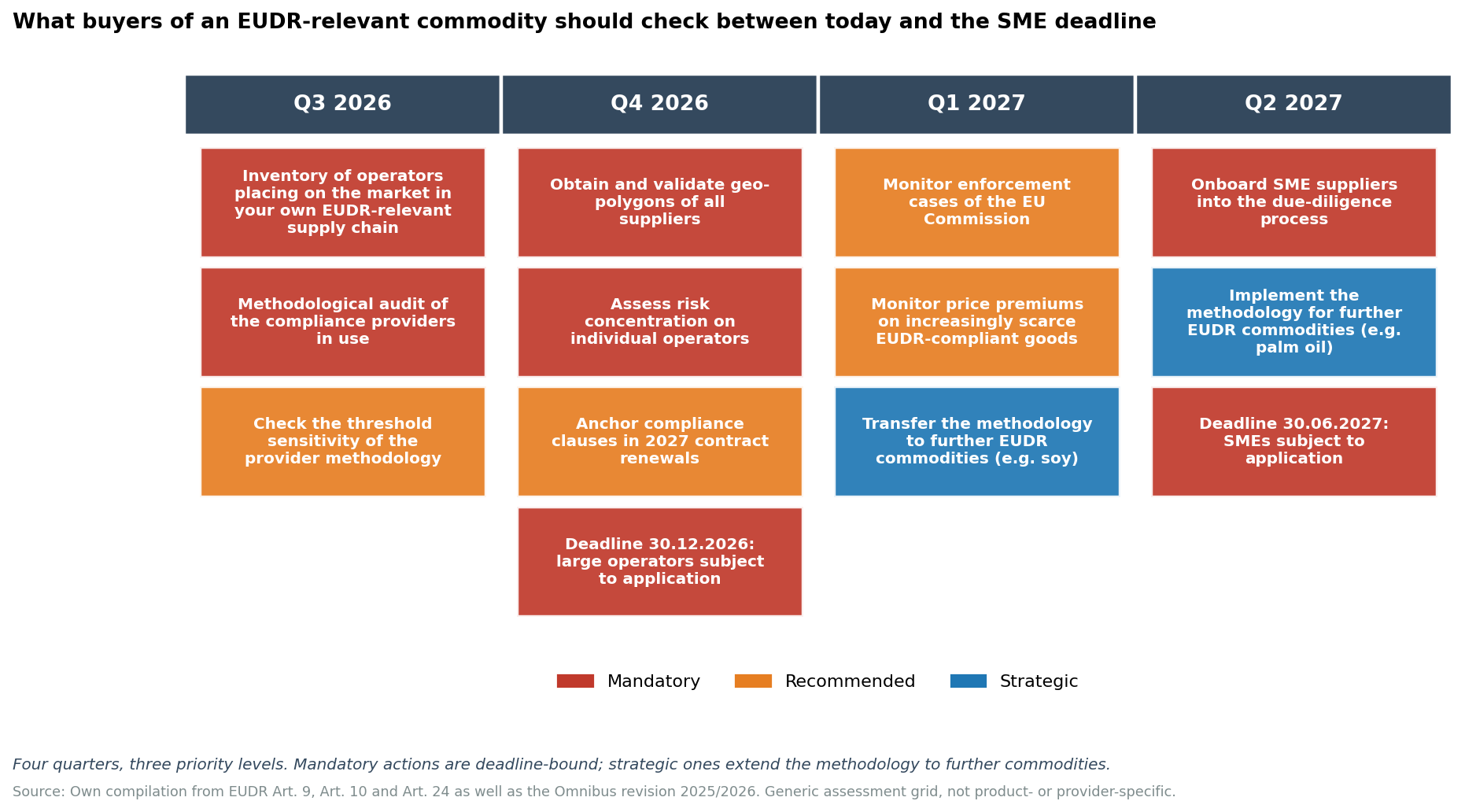

5 · What a six-month roadmap looks like today

Three quarters before the large-operator deadline, five before the SME deadline. The roadmap in the figure is formulated as a generic assessment grid for a mid-cap company with an EUDR-relevant supply chain. Cocoa serves only as an illustrative example from the regulation's seven-commodity list. It follows directly from the burden of proof under Article 10 and the first-placer concentration after the 2025/2026 Omnibus revision. Three observations that appear in no law-firm briefing:

The inventory of first placers in one's own supply chain must be completed in Q3 2026, not in Q4. A typical mid-cap group has, in an EUDR-relevant supply chain, usually between eight and fourteen first placers (in the cocoa sector, say, comparable in palm oil or soy). Mapping these cleanly is organizational work, not technical, and it blocks all downstream actions. Anyone who starts this in Q4 has no buffer for the negotiation phase with the first placers.

Checking the threshold sensitivity of the provider methodology in use is recommended in Q3, not mandatory. A provider who does not disclose the sensitivity of its τ threshold has either not implemented the procedure or not understood the results. In both cases this is a selection signal against the provider. A generic assessment grid for such provider audits is in the Truth-Check Protocol.

Transferring the methodology to further EUDR commodities is strategic, not mandatory. Anyone treating EUDR solely as a cocoa topic forfeits the methodological scale advantage that arises once the procedure is established. The two-mask operation works with Hansen combined with MapBiomas and Trase for Brazilian soy just as it does with Hansen combined with the FDP layer for cocoa. The data layers are interchangeable, the methodology is not.

6 · What we do not know

Six observation limits that honestly bound the picture above:

- How many operators will actually be hit in the first sanction round in 2027? We do not know. The Commission has not yet published a sanction pipeline.

- What market reaction to the first sanction cases is to be expected? We have scarcity-premium hypotheses, no empirical validation.

- We run the monitoring on public data layers. Operator polygons, the smallest relevant geographic unit under Article 9, are not available to us. Our Soubré/Sefwi-Wiawso risk shares are regionally aggregated, not delivery-polygon validated.

- A third EUDR postponement is not ruled out. Both postponements so far followed the same pattern: late in the year, an omnibus vehicle, a market reaction of “relief”. Anyone who pins the roadmap to the current deadlines can be surprised by a third wave.

- The 2026 CSDDD omnibus movement also shows: regulatory sustainability structures are in a phase of methodological self-calibration, not in a phase of final settlement. More changes are likely.

These six points are not defects of the work but the places where it is methodologically tested. Naming them openly is part of the methodology.

7 · Reading list & companion

The five most important sources for this article:

- EU Council, press release 18 December 2025, formal adoption of the second EUDR postponement.

- European Parliament, press release 17 December 2025. Vote result 405-242.

- Omnibus Directive (EU) 2026/470. CSDDD parallel simplification, Official Journal 26 February 2026.

- Regulation (EU) 2023/1115, the original EUDR, Article 2 (cut-off), Article 9 (geo obligation), Article 10 (risk assessment), Article 24 (enforcement), Article 25 (penalty framework).

- Hansen et al. 2013 Science and Kalischek et al. 2023 Nature Food, the methodological basis of our satellite monitoring.

Companion repository:

github.com/myBytesResearch/eudr-vintage-drift-2026,

a standalone snapshot of this article. The CSVs in data/runs/2026-06-08/ hold the vintage

comparison Hansen 2024 versus Hansen 2025 reproducibly and are the source of truth for the risk shares cited

above.

The associated methodology repository

github.com/myBytesResearch/eudr-risk-pipeline

contains the implementation of the two-mask operation described in the previous article.

Closing

For many market participants the second postponement was a relief; methodologically, however, it is above all an indication that the compliance world is looking for an answer it does not yet have in substance. The question is whether buyers, in the coming months, can distinguish methodologically clean providers from well-marketed ones.

Six months before the new deadline, the answer is not yet in. What is clear, though, is that the question is now being asked in procurement and no longer exclusively in the compliance department.

Disclaimer

This article summarizes the December 2025 EUDR revisions and the parallel 2026 CSDDD omnibus movement as the author understands them after his own research and as of June 2026. It does not replace legal advice. Cited article numbers, deadlines and thresholds are to be checked against the primary sources linked in the reading list. Binding statements on the compliance of your specific supply chain or on your position within the CSDDD scope require the involvement of competent legal counsel.Data and licence notes

The data layers used in Figure 2 follow different licences with different commercial-use conditions. The exact licence texts and the addresses for any clarification of commercial use are documented in the companion repositoryeudr-vintage-drift-2026

in the README.md and in each data/runs/<date>/README.md.